XAUUSD 10-Minute StrategyThis XAUUSD 10-Minute Strategy is designed for trading Gold vs. USD on a 10-minute timeframe. By combining multiple technical indicators (MACD, RSI, Bollinger Bands, and ATR), the strategy effectively captures both trend-following and reversal opportunities, with adaptive risk management for varying market volatility. This approach balances high-probability entries with robust volatility management, making it suitable for traders seeking to optimise entries during significant price movements and reversals.

Key Components and Logic:

MACD (12, 26, 9):

Generates buy signals on MACD Line crossovers above the Signal Line and sell signals on crossovers below the Signal Line, helping to capture momentum shifts.

RSI (14):

Utilizes oversold (below 35) and overbought (above 65) levels as a secondary filter to validate entries and avoid overextended price zones.

Bollinger Bands (20, 2):

Uses upper and lower Bollinger Bands to identify potential overbought and oversold conditions, aiming to enter long trades near the lower band and short trades near the upper band.

ATR-Based Stop Loss and Take Profit:

Stop Loss and Take Profit levels are dynamically set as multiples of ATR (3x for stop loss, 5x for take profit), ensuring flexibility with market volatility to optimise exit points.

Entry & Exit Conditions:

Buy Entry: T riggered when any of the following conditions are met:

MACD Line crosses above the Signal Line

RSI is oversold

Price drops below the lower Bollinger Band

Sell Entry: Triggered when any of the following conditions are met:

MACD Line crosses below the Signal Line

RSI is overbought

Price moves above the upper Bollinger Band

Exit Strategy: Trades are closed based on opposing entry signals, with adaptive spread adjustments for realistic exit points.

Backtesting Configuration & Results:

Backtesting Period: July 21, 2024, to October 30, 2024

Symbol Info: XAUUSD, 10-minute timeframe, OANDA data source

Backtesting Capital: Initial capital of $700, with each trade set to 10 contracts (equivalent to approximately 0.1 lots based on the broker’s contract size for gold).

Users should confirm their broker's contract size for gold, as this may differ. This script uses 10 contracts for backtesting purposes, aligned with 0.1 lots on brokers offering a 100-contract specification.

Key Backtesting Performance Metrics:

Net Profit: $4,733.90 USD (676.27% increase)

Total Closed Trades: 526

Win Rate: 53.99%

Profit Factor: 1.44 (1.96 for Long trades, 1.14 for Short trades)

Max Drawdown: $819.75 USD (56.33% of equity)

Sharpe Ratio: 1.726

Average Trade: $9.00 USD (0.04% of equity per trade)

This backtest reflects realistic conditions, with a spread adjustment of 38 points and no slippage or commission applied. The settings aim to simulate typical retail trading conditions. However, please adjust the initial capital, contract size, and other settings based on your account specifics for best results.

Usage:

This strategy is tuned specifically for XAUUSD on a 10-minute timeframe, ideal for both trend-following and reversal trades. The ATR-based stop loss and take profit levels adapt dynamically to market volatility, optimising entries and exits in varied conditions. To backtest this script accurately, ensure your broker’s contract specifications for gold align with the parameters used in this strategy.

Cari dalam skrip untuk "the strat"

Up/Down Volume with Normal DistributionThis indicator analyzes the relationship between price movements and trading volume by distinguishing between "up" and "down" volume. Up volume refers to trading volume occurring during price increases, while down volume refers to trading volume during price decreases. The indicator calculates the mean and standard deviation for both up and down volume over a specified length. This statistical approach enables traders to visualize volume deviations from the average, highlighting potential market anomalies that could signal trading opportunities.

Relationship Between Price and Volume

Volume is a critical metric in technical analysis, often considered a leading indicator of price movements. According to studies in financial economics, significant price changes accompanied by high volume tend to indicate strong market conviction (Wyart et al., 2008). Conversely, price changes on low volume may suggest a lack of interest or conviction, making those moves less reliable.

The relationship between price and volume can be summarized as follows:

Confirmation of Trends: High volume accompanying a price increase often confirms an upward trend. Similarly, high volume during price declines indicates bearish sentiment.

Reversals and Exhaustion: Decreases in volume during price increases may suggest a potential reversal or exhaustion of buying pressure, while increased volume during declines can indicate capitulation.

Breakouts: Price movements that break through significant resistance or support levels accompanied by high volume are typically more significant and suggest stronger follow-through in the new direction.

Developing a Trading Strategy

Traders can leverage the insights gained from this relationship to formulate a trading strategy based on volume analysis:

Entry Signals: Traders can enter long positions when the up volume significantly exceeds the mean by a predefined number of standard deviations. This situation indicates strong buying interest. Conversely, short positions can be initiated when down volume exceeds the mean by a specified standard deviation.

Exit Signals: Exiting positions can be based on changes in volume patterns. If the volume starts to decrease significantly after a price increase, this may signal a potential reversal or the need to lock in profits.

Risk Management: Integrating volume analysis with other technical indicators, such as moving averages or RSI, can provide a more comprehensive risk management framework, enhancing the overall effectiveness of the strategy.

In conclusion, understanding the relationship between price and volume, alongside employing statistical measures like the mean and standard deviation, enables traders to create more robust trading strategies that capitalize on market movements.

References

Wyart, M., Bouchaud, J.-P., & Dacorogna, M. (2008). "Self-organized volatility in a complicated market." European Physical Journal B, 61(2), 195-203. doi:10.1140

ICT Master Suite [Trading IQ]Hello Traders!

We’re excited to introduce the ICT Master Suite by TradingIQ, a new tool designed to bring together several ICT concepts and strategies in one place.

The Purpose Behind the ICT Master Suite

There are a few challenges traders often face when using ICT-related indicators:

Many available indicators focus on one or two ICT methods, which can limit traders who apply a broader range of ICT related techniques on their charts.

There aren't many indicators for ICT strategy models, and we couldn't find ICT indicators that allow for testing the strategy models and setting alerts.

Many ICT related concepts exist in the public domain as indicators, not strategies! This makes it difficult to verify that the ICT concept has some utility in the market you're trading and if it's worth trading - it's difficult to know if it's working!

Some users might not have enough chart space to apply numerous ICT related indicators, which can be restrictive for those wanting to use multiple ICT techniques simultaneously.

The ICT Master Suite is designed to offer a comprehensive option for traders who want to apply a variety of ICT methods. By combining several ICT techniques and strategy models into one indicator, it helps users maximize their chart space while accessing multiple tools in a single slot.

Additionally, the ICT Master Suite was developed as a strategy . This means users can backtest various ICT strategy models - including deep backtesting. A primary goal of this indicator is to let traders decide for themselves what markets to trade ICT concepts in and give them the capability to figure out if the strategy models are worth trading!

What Makes the ICT Master Suite Different

There are many ICT-related indicators available on TradingView, each offering valuable insights. What the ICT Master Suite aims to do is bring together a wider selection of these techniques into one tool. This includes both key ICT methods and strategy models, allowing traders to test and activate strategies all within one indicator.

Features

The ICT Master Suite offers:

Multiple ICT strategy models, including the 2022 Strategy Model and Unicorn Model, which can be built, tested, and used for live trading.

Calculation and display of key price areas like Breaker Blocks, Rejection Blocks, Order Blocks, Fair Value Gaps, Equal Levels, and more.

The ability to set alerts based on these ICT strategies and key price areas.

A comprehensive, yet practical, all-inclusive ICT indicator for traders.

Customizable Timeframe - Calculate ICT concepts on off-chart timeframes

Unicorn Strategy Model

2022 Strategy Model

Liquidity Raid Strategy Model

OTE (Optimal Trade Entry) Strategy Model

Silver Bullet Strategy Model

Order blocks

Breaker blocks

Rejection blocks

FVG

Strong highs and lows

Displacements

Liquidity sweeps

Power of 3

ICT Macros

HTF previous bar high and low

Break of Structure indications

Market Structure Shift indications

Equal highs and lows

Swings highs and swing lows

Fibonacci TPs and SLs

Swing level TPs and SLs

Previous day high and low TPs and SLs

And much more! An ongoing project!

How To Use

Many traders will already be familiar with the ICT related concepts listed above, and will find using the ICT Master Suite quite intuitive!

Despite this, let's go over the features of the tool in-depth and how to use the tool!

The image above shows the ICT Master Suite with almost all techniques activated.

ICT 2022 Strategy Model

The ICT Master suite provides the ability to test, set alerts for, and live trade the ICT 2022 Strategy Model.

The image above shows an example of a long position being entered following a complete setup for the 2022 ICT model.

A liquidity sweep occurs prior to an upside breakout. During the upside breakout the model looks for the FVG that is nearest 50% of the setup range. A limit order is placed at this FVG for entry.

The target entry percentage for the range is customizable in the settings. For instance, you can select to enter at an FVG nearest 33% of the range, 20%, 66%, etc.

The profit target for the model generally uses the highest high of the range (100%) for longs and the lowest low of the range (100%) for shorts. Stop losses are generally set at 0% of the range.

The image above shows the short model in action!

Whether you decide to follow the 2022 model diligently or not, you can still set alerts when the entry condition is met.

ICT Unicorn Model

The image above shows an example of a long position being entered following a complete setup for the ICT Unicorn model.

A lower swing low followed by a higher swing high precedes the overlap of an FVG and breaker block formed during the sequence.

During the upside breakout the model looks for an FVG and breaker block that formed during the sequence and overlap each other. A limit order is placed at the nearest overlap point to current price.

The profit target for this example trade is set at the swing high and the stop loss at the swing low. However, both the profit target and stop loss for this model are configurable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

For Longs, the selectable stop losses are:

Swing Low

Bottom of FVG or breaker block

The image above shows the short version of the Unicorn Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

For Shorts, the selectable stop losses are:

Swing High

Top of FVG or breaker block

The image above shows the profit target and stop loss options in the settings for the Unicorn Model.

Optimal Trade Entry (OTE) Model

The image above shows an example of a long position being entered following a complete setup for the OTE model.

Price retraces either 0.62, 0.705, or 0.79 of an upside move and a trade is entered.

The profit target for this example trade is set at the -0.5 fib level. This is also adjustable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

The image above shows the short version of the OTE Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

Liquidity Raid Model

The image above shows an example of a long position being entered following a complete setup for the Liquidity Raid Modell.

The user must define the session in the settings (for this example it is 13:30-16:00 NY time).

During the session, the indicator will calculate the session high and session low. Following a “raid” of either the session high or session low (after the session has completed) the script will look for an entry at a recently formed breaker block.

If the session high is raided the script will look for short entries at a bearish breaker block. If the session low is raided the script will look for long entries at a bullish breaker block.

For Longs, the profit target options are:

Swing high

User inputted Lib level

For Longs, the stop loss options are:

Swing low

User inputted Lib level

Breaker block bottom

The image above shows the short version of the Liquidity Raid Model in action!

For Shorts, the profit target options are:

Swing Low

User inputted Lib level

For Shorts, the stop loss options are:

Swing High

User inputted Lib level

Breaker block top

Silver Bullet Model

The image above shows an example of a long position being entered following a complete setup for the Silver Bullet Modell.

During the session, the indicator will determine the higher timeframe bias. If the higher timeframe bias is bullish the strategy will look to enter long at an FVG that forms during the session. If the higher timeframe bias is bearish the indicator will look to enter short at an FVG that forms during the session.

For Longs, the profit target options are:

Nearest Swing High Above Entry

Previous Day High

For Longs, the stop loss options are:

Nearest Swing Low

Previous Day Low

The image above shows the short version of the Silver Bullet Model in action!

For Shorts, the profit target options are:

Nearest Swing Low Below Entry

Previous Day Low

For Shorts, the stop loss options are:

Nearest Swing High

Previous Day High

Order blocks

The image above shows indicator identifying and labeling order blocks.

The color of the order blocks, and how many should be shown, are configurable in the settings!

Breaker Blocks

The image above shows indicator identifying and labeling order blocks.

The color of the breaker blocks, and how many should be shown, are configurable in the settings!

Rejection Blocks

The image above shows indicator identifying and labeling rejection blocks.

The color of the rejection blocks, and how many should be shown, are configurable in the settings!

Fair Value Gaps

The image above shows indicator identifying and labeling fair value gaps.

The color of the fair value gaps, and how many should be shown, are configurable in the settings!

Additionally, you can select to only show fair values gaps that form after a liquidity sweep. Doing so reduces "noisy" FVGs and focuses on identifying FVGs that form after a significant trading event.

The image above shows the feature enabled. A fair value gap that occurred after a liquidity sweep is shown.

Market Structure

The image above shows the ICT Master Suite calculating market structure shots and break of structures!

The color of MSS and BoS, and whether they should be displayed, are configurable in the settings.

Displacements

The images above show indicator identifying and labeling displacements.

The color of the displacements, and how many should be shown, are configurable in the settings!

Equal Price Points

The image above shows the indicator identifying and labeling equal highs and equal lows.

The color of the equal levels, and how many should be shown, are configurable in the settings!

Previous Custom TF High/Low

The image above shows the ICT Master Suite calculating the high and low price for a user-defined timeframe. In this case the previous day’s high and low are calculated.

To illustrate the customizable timeframe function, the image above shows the indicator calculating the previous 4 hour high and low.

Liquidity Sweeps

The image above shows the indicator identifying a liquidity sweep prior to an upside breakout.

The image above shows the indicator identifying a liquidity sweep prior to a downside breakout.

The color and aggressiveness of liquidity sweep identification are adjustable in the settings!

Power Of Three

The image above shows the indicator calculating Po3 for two user-defined higher timeframes!

Macros

The image above shows the ICT Master Suite identifying the ICT macros!

ICT Macros are only displayable on the 5 minute timeframe or less.

Strategy Performance Table

In addition to a full-fledged TradingView backtest for any of the ICT strategy models the indicator offers, a quick-and-easy strategy table exists for the indicator!

The image above shows the strategy performance table in action.

Keep in mind that, because the ICT Master Suite is a strategy script, you can perform fully automatic backtests, deep backtests, easily add commission and portfolio balance and look at pertinent metrics for the ICT strategies you are testing!

Lite Mode

Traders who want the cleanest chart possible can toggle on “Lite Mode”!

In Lite Mode, any neon or “glow” like effects are removed and key levels are marked as strict border boxes. You can also select to remove box borders if that’s what you prefer!

Settings Used For Backtest

For the displayed backtest, a starting balance of $1000 USD was used. A commission of 0.02%, slippage of 2 ticks, a verify price for limit orders of 2 ticks, and 5% of capital investment per order.

A commission of 0.02% was used due to the backtested asset being a perpetual future contract for a crypto currency. The highest commission (lowest-tier VIP) for maker orders on many exchanges is 0.02%. All entered positions take place as maker orders and so do profit target exits. Stop orders exist as stop-market orders.

A slippage of 2 ticks was used to simulate more realistic stop-market orders. A verify limit order settings of 2 ticks was also used. Even though BTCUSDT.P on Binance is liquid, we just want the backtest to be on the safe side. Additionally, the backtest traded 100+ trades over the period. The higher the sample size the better; however, this example test can serve as a starting point for traders interested in ICT concepts.

Community Assistance And Feedback

Given the complexity and idiosyncratic applications of ICT concepts amongst its proponents, the ICT Master Suite’s built-in strategies and level identification methods might not align with everyone's interpretation.

That said, the best we can do is precisely define ICT strategy rules and concepts to a repeatable process, test, and apply them! Whether or not an ICT strategy is trading precisely how you would trade it, seeing the model in action, taking trades, and with performance statistics is immensely helpful in assessing predictive utility.

If you think we missed something, you notice a bug, have an idea for strategy model improvement, please let us know! The ICT Master Suite is an ongoing project that will, ideally, be shaped by the community.

A big thank you to the @PineCoders for their Time Library!

Thank you!

Ultimate Oscillator Trading StrategyThe Ultimate Oscillator Trading Strategy implemented in Pine Script™ is based on the Ultimate Oscillator (UO), a momentum indicator developed by Larry Williams in 1976. The UO is designed to measure price momentum over multiple timeframes, providing a more comprehensive view of market conditions by considering short-term, medium-term, and long-term trends simultaneously. This strategy applies the UO as a mean-reversion tool, seeking to capitalize on temporary deviations from the mean price level in the asset’s movement (Williams, 1976).

Strategy Overview:

Calculation of the Ultimate Oscillator (UO):

The UO combines price action over three different periods (short-term, medium-term, and long-term) to generate a weighted momentum measure. The default settings used in this strategy are:

Short-term: 6 periods (adjustable between 2 and 10).

Medium-term: 14 periods (adjustable between 6 and 14).

Long-term: 20 periods (adjustable between 10 and 20).

The UO is calculated as a weighted average of buying pressure and true range across these periods. The weights are designed to give more emphasis to short-term momentum, reflecting the short-term mean-reversion behavior observed in financial markets (Murphy, 1999).

Entry Conditions:

A long position is opened when the UO value falls below 30, indicating that the asset is potentially oversold. The value of 30 is a common threshold that suggests the price may have deviated significantly from its mean and could be due for a reversal, consistent with mean-reversion theory (Jegadeesh & Titman, 1993).

Exit Conditions:

The long position is closed when the current close price exceeds the previous day’s high. This rule captures the reversal and price recovery, providing a defined point to take profits.

The use of previous highs as exit points aligns with breakout and momentum strategies, as it indicates sufficient strength for a price recovery (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages two well-established phenomena in financial markets: momentum and mean-reversion. Momentum, identified in earlier studies like those by Jegadeesh and Titman (1993), describes the tendency of assets to continue in their direction of movement over short periods. Mean-reversion, as discussed by Poterba and Summers (1988), indicates that asset prices tend to revert to their mean over time after short-term deviations. This dual approach aims to buy assets when they are temporarily oversold and capitalize on their return to the mean.

Multi-timeframe Analysis:

The UO’s incorporation of multiple timeframes (short, medium, and long) provides a holistic view of momentum, unlike single-period oscillators such as the RSI. By combining data across different timeframes, the UO offers a more robust signal and reduces the risk of false entries often associated with single-period momentum indicators (Murphy, 1999).

Trading and Market Efficiency:

Studies in behavioral finance, such as those by Shiller (2003), show that short-term inefficiencies and behavioral biases can lead to overreactions in the market, resulting in price deviations. This strategy seeks to exploit these temporary inefficiencies, using the UO as a signal to identify potential entry points when the market sentiment may have overly pushed the price away from its average.

Strategy Performance:

Backtests of this strategy show promising results, with profit factors exceeding 2.5 when the default settings are optimized. These results are consistent with other studies on short-term trading strategies that capitalize on mean-reversion patterns (Jegadeesh & Titman, 1993). The use of a dynamic, multi-period indicator like the UO enhances the strategy’s adaptability, making it effective across different market conditions and timeframes.

Conclusion:

The Ultimate Oscillator Trading Strategy effectively combines momentum and mean-reversion principles to trade on temporary market inefficiencies. By utilizing multiple periods in its calculation, the UO provides a more reliable and comprehensive measure of momentum, reducing the likelihood of false signals and increasing the profitability of trades. This aligns with modern financial research, showing that strategies based on mean-reversion and multi-timeframe analysis can be effective in capturing short-term price movements.

References:

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1976). Ultimate Oscillator. Market research and technical trading analysis.

VIDYA ProTrend Multi-Tier ProfitHello! This time is about a trend-following system.

VIDYA is quite an interesting indicator that adjusts dynamically to market volatility, making it more responsive to price changes compared to traditional moving averages. Balancing adaptability and precision, especially with the more aggressive short trade settings, challenged me to fine-tune the strategy for a variety of market conditions.

█ Introduction and How it is Different

The "VIDYA ProTrend Multi-Tier Profit" strategy is a trend-following system that combines the VIDYA (Variable Index Dynamic Average) indicator with Bollinger Bands and a multi-step take-profit mechanism.

Unlike traditional trend strategies, this system allows for more adaptive profit-taking, adjusting for long and short positions through distinct ATR-based and percentage-based targets. The innovation lies in its dynamic multi-tier approach to profit-taking, especially for short trades, where more aggressive percentages are applied using a multiplier. This flexibility helps adapt to various market conditions by optimizing trade management and profit allocation based on market volatility and trend strength.

BTCUSD 6hr performance

█ Strategy, How it Works: Detailed Explanation

The core of the "VIDYA ProTrend Multi-Tier Profit" strategy lies in the dual VIDYA indicators (fast and slow) that analyze price trends while accounting for market volatility. These indicators work alongside Bollinger Bands to filter trade entries and exits.

🔶 VIDYA Calculation

The VIDYA indicator is calculated using the following formula:

Smoothing factor (𝛼):

alpha = 2 / (Length + 1)

VIDYA formula:

VIDYA(t) = alpha * k * Price(t) + (1 - alpha * k) * VIDYA(t-1)

Where:

k = |Chande Momentum Oscillator (MO)| / 100

🔶 Bollinger Bands as a Volatility Filter

Bollinger Bands are calculated using a rolling mean and standard deviation of price over a specified period:

Upper Band:

BB_upper = MA + (K * stddev)

Lower Band:

BB_lower = MA - (K * stddev)

Where:

MA is the moving average,

K is the multiplier (typically 2), and

stddev is the standard deviation of price over the Bollinger Bands length.

These bands serve as volatility filters to identify potential overbought or oversold conditions, aiding in the entry and exit logic.

🔶 Slope Calculation for VIDYA

The slopes of both fast and slow VIDYAs are computed to assess the momentum and direction of the trend. The slope for a given VIDYA over its length is:

Slope = (VIDYA(t) - VIDYA(t-n)) / n

Where:

n is the length of the lookback period. Positive slope indicates bullish momentum, while negative slope signals bearish momentum.

LOCAL picture

🔶 Entry and Exit Conditions

- Long Entry: Occurs when the price moves above the slow VIDYA and the fast VIDYA is trending upward. Bollinger Bands confirm the signal when the price crosses the upper band, indicating bullish strength.

- Short Entry: Happens when the price drops below the slow VIDYA and the fast VIDYA trends downward. The signal is confirmed when the price crosses the lower Bollinger Band, showing bearish momentum.

- Exit: Based on VIDYA slopes flattening or reversing, or when the price hits specific ATR or percentage-based profit targets.

🔶 Multi-Step Take Profit Mechanism

The strategy incorporates three levels of take profit for both long and short trades:

- ATR-based Take Profit: Each step applies a multiple of the ATR (Average True Range) to the entry price to define the exit point.

The first level of take profit (long):

TP_ATR1_long = Entry Price + (2.618 * ATR)

etc.

█ Trade Direction

The strategy offers flexibility in defining the trading direction:

- Long: Only long trades are considered based on the criteria for upward trends.

- Short: Only short trades are initiated in bearish trends.

- Both: The strategy can take both long and short trades depending on the market conditions.

█ Usage

To use the strategy effectively:

- Adjust the VIDYA lengths (fast and slow) based on your preference for trend sensitivity.

- Use Bollinger Bands as a filter for identifying potential breakout or reversal scenarios.

- Enable the multi-step take profit feature to manage positions dynamically, allowing for partial exits as the price reaches specified ATR or percentage levels.

- Leverage the short trade multiplier for more aggressive take profit levels in bearish markets.

This strategy can be applied to different asset classes, including equities, forex, and cryptocurrencies. Adjust the input parameters to suit the volatility and characteristics of the asset being traded.

█ Default Settings

The default settings for this strategy have been designed for moderate to trending markets:

- Fast VIDYA Length (10): A shorter length for quick responsiveness to price changes. Increasing this length will reduce noise but may delay signals.

- Slow VIDYA Length (30): The slow VIDYA is set longer to capture broader market trends. Shortening this value will make the system more reactive to smaller price swings.

- Minimum Slope Threshold (0.05): This threshold helps filter out weak trends. Lowering the threshold will result in more trades, while raising it will restrict trades to stronger trends.

Multi-Step Take Profit Settings

- ATR Multipliers (2.618, 5.0, 10.0): These values define how far the price should move before taking profit. Larger multipliers widen the profit-taking levels, aiming for larger trend moves. In higher volatility markets, these values might be adjusted downwards.

- Percentage Levels (3%, 8%, 17%): These percentage levels define how much the price must move before taking profit. Increasing the percentages will capture larger moves, while smaller percentages offer quicker exits.

- Short TP Multiplier (1.5): This multiplier applies more aggressive take profit levels for short trades. Adjust this value based on the aggressiveness of your short trade management.

Each of these settings directly impacts the performance and risk profile of the strategy. Shorter VIDYA lengths and lower slope thresholds will generate more trades but may result in more whipsaws. Higher ATR multipliers or percentage levels can delay profit-taking, aiming for larger trends but risking partial gains if the trend reverses too early.

Fibonacci & Bollinger Bands StrategyThis strategy combines Bollinger Bands and Fibonacci retracement/extension levels to identify potential entry and exit points in the market. Here’s a breakdown of each component and how the strategy works:

1. Bollinger Bands:

Bollinger Bands consist of a simple moving average (SMA) and two standard deviations (upper and lower bands) plotted above and below the SMA. The bands expand and contract based on market volatility.

Purpose in Strategy:

The lower band represents an area where the market might be oversold.

The upper band represents an area where the market might be overbought.

The price crossing these bands suggests overextended market conditions, which can be used to identify potential reversals.

2. Fibonacci Retracement and Extension Levels:

Fibonacci retracement levels are horizontal lines that indicate where price might find support or resistance as it retraces some of its previous movement. Common retracement levels are 61.8% and 78.6%.

Fibonacci extension levels are used to project areas where the price might extend after completing a retracement. These levels can help determine potential targets after a significant price movement.

Purpose in Strategy:

The strategy calculates the most recent swing high (fibHigh) and swing low (fibLow) over a lookback period. It then plots Fibonacci retracement and extension levels based on this range.

The Fibonacci levels are used as key support and resistance areas. The price approaching or touching these levels signals potential turning points in the market.

3. Entry Criteria:

A long position (buy) is triggered when:

The price crosses below the lower Bollinger Band, indicating an oversold condition.

The price is near or above a Fibonacci extension level (calculated based on the most recent price swing).

This suggests that the price is potentially reaching a strong support area, where a reversal is likely.

4. Exit Criteria:

The long position is closed (exit trade) when either:

The price touches or crosses the upper Bollinger Band, signaling an overbought condition.

The price reaches a Fibonacci retracement level or exceeds the recent swing high (fibHigh), indicating a potential exhaustion point or a reversal area.

5. General Strategy Logic:

The strategy takes advantage of market volatility (captured by the Bollinger Bands) and key support/resistance levels (determined by Fibonacci retracement and extension levels).

By combining these two techniques, the strategy identifies potential entry points at oversold levels with the expectation that the market will retrace or reverse upward, especially when near key Fibonacci extension levels.

Exit points are identified by potential overbought levels (Bollinger upper band) or key Fibonacci retracement levels, where the price might reverse downward.

6. Conditions to Execute the Strategy:

The Fibonacci levels are only calculated once the price has made a significant movement, establishing a recent high and low over a 50-bar period (which you can adjust). This ensures the Fibonacci levels are based on meaningful swings.

The entry and exit signals are filtered using both Bollinger Bands and Fibonacci levels to ensure that trades are not taken solely based on one indicator, thus reducing false signals.

Key Features of the Strategy:

Trend-following with reversal: It tries to catch reversals when the price hits extreme levels (Bollinger Bands) while respecting important Fibonacci levels.

Dynamic market adaptation: The strategy adapts to market conditions as it recalculates Fibonacci levels based on recent price swings and adjusts the Bollinger Bands for market volatility.

Confirmation through multiple indicators: It uses both the volatility-based signals from Bollinger Bands and the price structure from Fibonacci levels to confirm trade entries and exits.

Summary of the Strategy:

The strategy looks to buy low and sell high based on oversold/overbought signals from Bollinger Bands and Fibonacci levels that indicate key support and resistance zones.

By combining these two technical indicators, the strategy aims to reduce risk and increase accuracy by only entering trades when both indicators suggest favorable conditions.

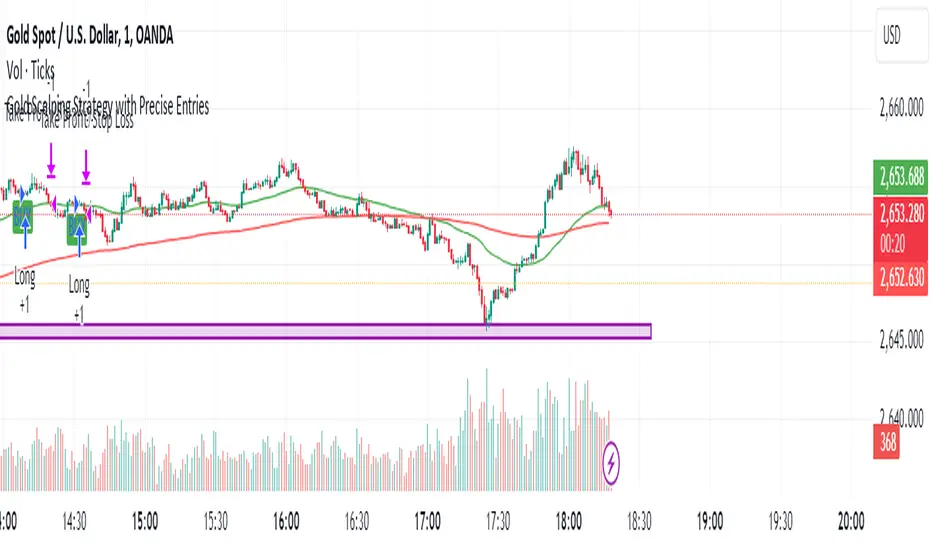

Gold Scalping Strategy with Precise EntriesThe Gold Scalping Strategy with Precise Entries is designed to take advantage of short-term price movements in the gold market (XAU/USD). This strategy uses a combination of technical indicators and chart patterns to identify precise buy and sell opportunities during times of consolidation and trend continuation.

Key Elements of the Strategy:

Exponential Moving Averages (EMAs):

50 EMA: Used as the shorter-term moving average to detect the recent price trend.

200 EMA: Used as the longer-term moving average to determine the overall market trend.

Trend Identification:

A bullish trend is identified when the 50 EMA is above the 200 EMA.

A bearish trend is identified when the 50 EMA is below the 200 EMA.

Average True Range (ATR):

ATR (14) is used to calculate the market's volatility and to set a dynamic stop loss based on recent price movements. Higher ATR values indicate higher volatility.

ATR helps define a suitable stop-loss distance from the entry point.

Relative Strength Index (RSI):

RSI (14) is used as a momentum oscillator to detect overbought or oversold conditions.

However, in this strategy, the RSI is primarily used as a consolidation filter to look for neutral zones (between 45 and 55), which may indicate a potential breakout or trend continuation after a consolidation phase.

Engulfing Patterns:

Bullish Engulfing: A bullish signal is generated when the current candle fully engulfs the previous bearish candle, indicating potential upward momentum.

Bearish Engulfing: A bearish signal is generated when the current candle fully engulfs the previous bullish candle, signaling potential downward momentum.

Precise Entry Conditions:

Long (Buy):

The 50 EMA is above the 200 EMA (bullish trend).

The RSI is between 45 and 55 (neutral/consolidation zone).

A bullish engulfing pattern occurs.

The price closes above the 50 EMA.

Short (Sell):

The 50 EMA is below the 200 EMA (bearish trend).

The RSI is between 45 and 55 (neutral/consolidation zone).

A bearish engulfing pattern occurs.

The price closes below the 50 EMA.

Take Profit and Stop Loss:

Take Profit: A fixed 20-pip target (where 1 pip = 0.10 movement in gold) is used for each trade.

Stop Loss: The stop-loss is dynamically set based on the ATR, ensuring that it adapts to current market volatility.

Visual Signals:

Buy and sell signals are visually plotted on the chart using green and red labels, indicating precise points of entry.

Advantages of This Strategy:

Trend Alignment: The strategy ensures that trades are taken in the direction of the overall trend, as indicated by the 50 and 200 EMAs.

Volatility Adaptation: The use of ATR allows the stop loss to adapt to the current market conditions, reducing the risk of premature exits in volatile markets.

Precise Entries: The combination of engulfing patterns and the neutral RSI zone provides a high-probability entry signal that captures momentum after consolidation.

Quick Scalping: With a fixed 20-pip profit target, the strategy is designed to capture small price movements quickly, which is ideal for scalping.

This strategy can be applied to lower timeframes (such as 1-minute, 5-minute, or 15-minute charts) for frequent trade opportunities in gold trading, making it suitable for day traders or scalpers. However, proper risk management should always be used due to the inherent volatility of gold.

D_Rock's MA IndicatorD_Rock's Moving Average Indicator

This is an indicator version of my strategy linked here

**Overview:**

The basic concept of this indicator is to generate a signal when a faster/shorter length moving average crosses over (for Longs) or crosses under (for Shorts) a medium/longer length moving average. All of which are customizable. This indicator can work on any timeframe, however the daily is the timeframe used for the default settings and screenshots, as it was designed to be a multi-day swing strategy. Once a signal has been confirmed with a candle close, based on user options, the strategy is to enter the trade on the open of the next candle.

The crossover strategy is nothing new to trading, but what can make this strategy unique and helpful, is the addition of further confirmation points before a signal is generated along with the ability to show multiple moving averages on the chart if you choose. Each moving average pair can also be turned into a "cloud" instead of the traditional lines, for additional viewing preferences. Just about everything visual can be toggled on/off as well.

This indicator is a Trend (MA) indicator with optional confirmation points using a Momentum (MACD) indicator. While a Volume-based indicator is not shown here, one could consider using their favorite from that category to further compliment the signal idea.

If you would like to see the backtesting results for your favorite moving average crossover/under, please see my strategy version linked here .

Shoutout given to Ripster's Clouds Indicator as pieces of that code were taken and modified to create both the Cloud visualization effects, and the Moving Average Pair Plots that are implemented in this strategy.

MOVING AVERAGE OPTIONS

Select between and change the length & type of up to 5 pairs (10 total) of moving averages

The "Show Cloud-x" option will display a fill color between the "a" and "b" pairs

All moving averages lines can be toggled on/off in the "Style" tab, as well as adjusting their colors.

Visualization features do not affect calculations, meaning you could have all or nothing on the chart and the strategy will still produce results

SIGNAL CHOICES

Choose the fast/shorter length MA and the medium/longer length MA to determine the entry signal

CONFIRMATION OPTIONS

Both of these have customizable values and can be toggled on/off

A candle close over a slower/much longer length moving average

An additional cross-over (cross-under for Shorts) on the MACD indicator using default MACD values. While the MACD indicator is not necessary to have on the chart, it can help to add that for visualization. The calculations will perform whether the indicator is on the chart or not.

ADDITIONAL PLOTS

MACD (Moving Average Convergence/Divergence):

- The MACD is an optional confirmation indicator for this strategy.

- Plotting the indicator is not necessary for the strategy to work, but it can be helpful to visually see the status and position of the MACD if this feature is enabled in the strategy

- This helps to identify if there is also momentum behind the entry signal

ADX + Volume Strategy### Strategy Description: ADX and Volume-Based Trading Strategy

This strategy is designed to identify strong market trends using the **Average Directional Index (ADX)** and confirm trading signals with **Volume**. The idea behind the strategy is to enter trades only when the market shows a strong trend (as indicated by ADX) and when the price movement is supported by high trading volume. This combination helps filter out weaker signals and provides more reliable entries into positions.

### Key Indicators:

1. **ADX (Average Directional Index)**:

- **Purpose**: ADX is a technical indicator that measures the strength of a trend, regardless of its direction (up or down).

- **Usage**: The strategy uses ADX to determine whether the market is trending strongly. If ADX is above a certain threshold (default is 25), it indicates that a strong trend is present.

- **Directional Indicators**:

- **DI+ (Directional Indicator Plus)**: Indicates the strength of the upward price movement.

- **DI- (Directional Indicator Minus)**: Indicates the strength of the downward price movement.

- ADX does not indicate the direction of the trend but confirms that a trend exists. DI+ and DI- are used to determine the direction.

2. **Volume**:

- **Purpose**: Volume is a key indicator for confirming the strength of a price movement. High volume suggests that a large number of market participants are supporting the movement, making it more likely to continue.

- **Usage**: The strategy compares the current volume to the 20-period moving average of the volume. The trade signal is confirmed if the current volume is greater than the average volume by a specified **Volume Multiplier** (default multiplier is 1.5). This ensures that the trade is supported by strong market participation.

### Strategy Logic:

#### **Entry Conditions:**

1. **Long Position** (Buy):

- **ADX** is above the threshold (default is 25), indicating a strong trend.

- **DI+ > DI-**, signaling that the market is trending upward.

- The **current volume** is greater than the 20-period average volume multiplied by the **Volume Multiplier** (e.g., 1.5), indicating that the upward price movement is backed by sufficient market activity.

2. **Short Position** (Sell):

- **ADX** is above the threshold (default is 25), indicating a strong trend.

- **DI- > DI+**, signaling that the market is trending downward.

- The **current volume** is greater than the 20-period average volume multiplied by the **Volume Multiplier** (e.g., 1.5), indicating that the downward price movement is backed by strong selling activity.

#### **Exit Conditions**:

- Positions are closed when the opposite signal appears:

- **For long positions**: Close when the short conditions are met (ADX still above the threshold, DI- > DI+, and the volume condition holds).

- **For short positions**: Close when the long conditions are met (ADX still above the threshold, DI+ > DI-, and the volume condition holds).

### Parameters:

- **ADX Period**: The period used to calculate ADX (default is 14). This controls how sensitive the ADX is to price movements.

- **ADX Threshold**: The minimum ADX value required for the strategy to consider the market trend as strong (default is 25). Higher values focus on stronger trends.

- **Volume Multiplier**: This parameter adjusts how much higher the current volume needs to be compared to the 20-period moving average for the signal to be valid. A value of 1.5 means the current volume must be 50% higher than the average volume.

### Example Trade Flow:

1. **Long Trade Example**:

- ADX > 25, confirming a strong trend.

- DI+ > DI-, confirming that the trend direction is upward.

- The current volume is 50% higher than the 20-period average volume (multiplied by 1.5).

- **Action**: Enter a long position.

2. **Short Trade Example**:

- ADX > 25, confirming a strong trend.

- DI- > DI+, confirming that the trend direction is downward.

- The current volume is 50% higher than the 20-period average volume.

- **Action**: Enter a short position.

### Strengths of the Strategy:

- **Trend Filtering**: The strategy ensures that trades are only taken when the market is trending strongly (confirmed by ADX) and that the price movement is supported by high volume, reducing the likelihood of false signals.

- **Volume Confirmation**: Using volume as confirmation provides an additional layer of reliability, as volume spikes often accompany sustained price moves.

- **Dual Signal Confirmation**: Both trend strength (ADX) and volume conditions must be met for a trade, making the strategy more robust.

### Weaknesses of the Strategy:

- **Limited Effectiveness in Range-Bound Markets**: Since the strategy relies on strong trends, it may underperform in sideways or non-trending markets where ADX stays below the threshold.

- **Lagging Nature of ADX**: ADX is a lagging indicator, which means that it may confirm the trend after it has already begun, potentially leading to late entries.

- **Volume Requirement**: In low-volume markets, the volume multiplier condition may not be met often, leading to fewer trade opportunities.

### Customization:

- **Adjust the ADX Threshold**: You can raise the threshold if you want to focus only on very strong trends, or lower it to capture moderate trends.

- **Adjust the Volume Multiplier**: You can change the multiplier to be more or less strict. A higher multiplier (e.g., 2.0) will require a stronger volume spike to confirm the signal, while a lower multiplier (e.g., 1.2) will allow more trades with weaker volume confirmation.

### Summary:

This ADX and Volume strategy is ideal for traders who want to follow strong trends while ensuring that the trend is supported by high trading volume. By combining a trend strength filter (ADX) and volume confirmation, the strategy aims to increase the probability of entering profitable trades while reducing the number of false signals. However, it may underperform in range-bound markets or in markets with low volume.

analytics_tablesLibrary "analytics_tables"

📝 Description

This library provides the implementation of several performance-related statistics and metrics, presented in the form of tables.

The metrics shown in the afforementioned tables where developed during the past years of my in-depth analalysis of various strategies in an atempt to reason about the performance of each strategy.

The visualization and some statistics where inspired by the existing implementations of the "Seasonality" script, and the performance matrix implementations of @QuantNomad and @ZenAndTheArtOfTrading scripts.

While this library is meant to be used by my strategy framework "Template Trailing Strategy (Backtester)" script, I wrapped it in a library hoping this can be usefull for other community strategy scripts that will be released in the future.

🤔 How to Guide

To use the functionality this library provides in your script you have to import it first!

Copy the import statement of the latest release by pressing the copy button below and then paste it into your script. Give a short name to this library so you can refer to it later on. The import statement should look like this:

import jason5480/analytics_tables/1 as ant

There are three types of tables provided by this library in the initial release. The stats table the metrics table and the seasonality table.

Each one shows different kinds of performance statistics.

The table UDT shall be initialized once using the `init()` method.

They can be updated using the `update()` method where the updated data UDT object shall be passed.

The data UDT can also initialized and get updated on demend depending on the use case

A code example for the StatsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(SideStats.new(), SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var statsTable = ant.StatsTable.new().init(ant.getTablePos('TOP', 'RIGHT'))

statsTable.update(statsData)

A code example for the MetricsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(ant.SideStats.new(), ant.SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var metricsTable = ant.MetricsTable.new().init(ant.getTablePos('BOTTOM', 'RIGHT'))

metricsTable.update(statsData, 10)

A code example for the SeasonalityTable is the following:

var ant.SeasonalData seasonalData = ant.SeasonalData.new().init(Seasonality.monthOfYear)

seasonalData.update()

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var seasonalTable = ant.SeasonalTable.new().init(seasonalData, ant.getTablePos('BOTTOM', 'LEFT'))

seasonalTable.update(seasonalData)

🏋️♂️ Please refer to the "EXAMPLE" regions of the script for more advanced and up to date code examples!

Special thanks to @Mrcrbw for the proposal to develop this library and @DCNeu for the constructive feedback 🏆.

getTablePos(ypos, xpos)

Get table position compatible string

Parameters:

ypos (simple string) : The position on y axise

xpos (simple string) : The position on x axise

Returns: The position to be passed to the table

method init(this, pos, height, width, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor)

Initialize the stats table object with the given colors in the given position

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts height. By default, 0 auto-adjusts the width based on the text inside the cells

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, pos, height, width, neutralBgColor)

Initialize the metrics table object with the given colors in the given position

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, seas)

Initialize the seasonal data

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

seas (simple Seasonality) : The seasonality of the matrix data

method init(this, data, pos, maxNumOfYears, height, width, extended, neutralTxtColor, neutralBgColor)

Initialize the seasonal table object with the given colors in the given position

Namespace types: SeasonalTable

Parameters:

this (SeasonalTable) : The seasonal table object

data (SeasonalData) : The seasonality data of the table

pos (simple string) : The table position string

maxNumOfYears (simple int) : The maximum number of years that fit into the table

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

extended (simple bool) : The seasonal table with extended columns for performance

neutralTxtColor (simple color) : The text color when neutral

neutralBgColor (simple color) : The background color with transparency when neutral

method update(this, wins, losses, numOfInconclusiveExits)

Update the strategy info data of the strategy

Namespace types: StatsData

Parameters:

this (StatsData) : The strategy statistics object

wins (SideStats)

losses (SideStats)

numOfInconclusiveExits (int) : The number of inconclusive trades

method update(this, stats, positiveTxtColor, negativeTxtColor, negativeBgColor, neutralBgColor)

Update the stats table object with the given data

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

stats (StatsData) : The stats data to update the table

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method update(this, stats, buyAndHoldPerc, positiveTxtColor, negativeTxtColor, positiveBgColor, negativeBgColor)

Update the metrics table object with the given data

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

stats (StatsData) : The stats data to update the table

buyAndHoldPerc (float) : The buy and hold percetage

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

method update(this)

Update the seasonal data based on the season and eon timeframe

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

method update(this, data, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor, timeBgColor)

Update the seasonal table object with the given data

Namespace types: SeasonalTable

Parameters:

this (SeasonalTable) : The seasonal table object

data (SeasonalData) : The seasonal cell data to update the table

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

timeBgColor (simple color) : The background color of the time gradient

SideStats

Object that represents the strategy statistics data of one side win or lose

Fields:

numOf (series int)

sumFreeProfit (series float)

freeProfitStDev (series float)

sumProfit (series float)

profitStDev (series float)

sumGain (series float)

gainStDev (series float)

avgQuantityPerc (series float)

avgCapitalRiskPerc (series float)

avgTPExecutedCount (series float)

avgRiskRewardRatio (series float)

maxStreak (series int)

StatsTable

Object that represents the stats table

Fields:

table (series table) : The actual table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

StatsData

Object that represents the statistics data of the strategy

Fields:

wins (SideStats)

losses (SideStats)

numOfInconclusiveExits (series int)

avgFreeProfitStr (series string)

freeProfitStDevStr (series string)

lossFreeProfitStDevStr (series string)

avgProfitStr (series string)

profitStDevStr (series string)

lossProfitStDevStr (series string)

avgQuantityStr (series string)

MetricsTable

Object that represents the metrics table

Fields:

table (series table) : The actual table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

SeasonalData

Object that represents the seasonal table dynamic data

Fields:

seasonality (series Seasonality)

eonToMatrixRow (map)

numOfEons (series int)

mostRecentMatrixRow (series int)

balances (matrix)

returnPercs (matrix)

maxDDs (matrix)

eonReturnPercs (array)

eonCAGRs (array)

eonMaxDDs (array)

SeasonalTable

Object that represents the seasonal table

Fields:

table (series table) : The actual table

headRows (series int) : The number of head rows of the table

headColumns (series int) : The number of head columns of the table

eonRows (series int) : The number of eon rows of the table

seasonColumns (series int) : The number of season columns of the table

statsRows (series int)

statsColumns (series int) : The number of stats columns of the table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

extended (series bool) : Whether the table has additional performance statistics

Simultaneous INSIDE Bar Break IndicatorSimultaneous Inside Bar Break Indicator (SIBBI) for The Strat Community

Overview:

The Simultaneous Inside Bar Break Indicator (SIBBI) is designed to help traders using The Strat methodology identify one of the most powerful breakout patterns: the Simultaneous Inside Bar Break across multiple symbols. This indicator detects when all four user-selected symbols form inside bars on the previous candle and then break those inside bars in the same direction (either bullish or bearish) on the current candle.

Inside bars represent consolidation periods where price action does not break the high or low of the previous candle. When a simultaneous break occurs across multiple symbols, this often signals a strong move in the market, making this a key actionable signal in The Strat trading strategy.

Key Features:

Multi-Symbol Analysis: You can track up to four different symbols simultaneously. By default, the indicator comes with SPY, QQQ, IWM, and DIA, but you can modify these to track any other assets or symbols.

Inside Bar Detection: The indicator checks whether all four symbols have inside bars on the previous candle. It only triggers when all symbols meet this condition, making it a highly specific and reliable signal.

Simultaneous Break Detection: Once all symbols have inside bars, the indicator waits for a breakout in the same direction across all four symbols. A simultaneous bullish break (prices breaking above the previous candle’s high) triggers a green label, while a simultaneous bearish break (prices breaking below the previous candle’s low) triggers a red label.

Dynamic Label Timeframe: The indicator dynamically adjusts the timeframe in the label based on the user’s selected timeframe. This allows traders to know precisely which timeframe the break is occurring on. If the user selects "Chart Timeframe," the indicator will evolve with the current chart's timeframe, making it more versatile.

Timeframe Flexibility: The indicator can be set to analyze any timeframe—15-minute, 30-minute, 60-minute, daily, weekly, and so on. It only works for the specific timeframe you set it to in the settings. If set to "Chart Timeframe," the label will adapt dynamically based on the timeframe you are currently viewing.

Customizable Labels: The user can choose the size of the labels (tiny, small, or normal), ensuring that the visual output is tailored to individual preferences and chart layouts.

Best Use Case:

The Simultaneous Inside Bar Break Indicator is particularly powerful when applied to multiple timeframes. Here’s how to use it for maximum impact:

Multi-Timeframe Setup: Set the indicator on various timeframes (e.g., 15-minute, 30-minute, 60-minute, and daily) across multiple charts. This allows you to monitor different timeframes and identify when lower timeframe breaks trigger potential moves on higher timeframes.

Anticipating Strong Moves: When a simultaneous inside bar break occurs on one timeframe (e.g., 30-minute), keep an eye on the higher timeframes (e.g., 60-minute or daily) to see if those timeframes also break. This stacking of inside bar breaks can signal powerful market moves.

Higher Conviction Signals: The indicator is designed to provide high-conviction signals. Since it requires all four symbols to break in the same direction simultaneously, it reduces false signals and focuses on higher probability setups, which is crucial for traders using The Strat to time their trades effectively.

How the Indicator Works:

Inside Bar Formation: The indicator first checks that all four selected symbols had inside bars in the previous bar (i.e., the current high and low are contained within the previous bar’s high and low).

Simultaneous Break Detection: After detecting inside bars, the indicator checks if all four symbols break out in the same direction—bullish (breaking above the previous bar’s high) or bearish (breaking below the previous bar’s low).

Label Display: When a simultaneous inside bar break occurs, a label is plotted on the chart—either green for a bullish break (below the candle) or red for a bearish break (above the candle). The label will display the timeframe you set in the settings (e.g., "IBSB 60" for a 60-minute break).

Chart Timeframe Option: If you prefer, you can set the indicator to evolve with the chart’s current timeframe. In this mode, the label will not show a specific timeframe but will still display the simultaneous inside bar break when it occurs.

Recommendations for Usage:

Focus on Multiple Timeframes: The Strat methodology is all about understanding the relationship between different timeframes. Use this indicator on multiple timeframes to get a better picture of potential moves.

Pair with Other Strat Techniques: This indicator is most powerful when combined with other Strat tools, such as broadening formations, timeframe continuity, and actionable signals (e.g., 2-2 reversals). The simultaneous inside bar break can help confirm or invalidate other signals.

Customize Symbols and Timeframes: Although the default symbols are SPY, QQQ, IWM, and DIA, feel free to replace them with symbols more relevant to your trading. This indicator works well across equities, indices, futures, and forex pairs.

How to Set It Up:

Select Symbols: Choose four symbols that you want to track. These can be index ETFs (like SPY and QQQ), individual stocks, or any other tradable instruments.

Set Timeframe: In the indicator’s settings, choose a specific timeframe (e.g., 15-minute, 30-minute, daily). The label will reflect the selected timeframe, making it clear which time-based break you are seeing.

Optional - Chart Timeframe Mode: If you want the indicator to adapt to the chart’s current timeframe, select the "Chart Timeframe" option in the settings. The indicator will plot the breaks without showing a specific timeframe in the label.

Customize Label Size: Depending on your chart layout and personal preference, you can adjust the size of the labels (tiny, small, or normal) in the settings.

Conclusion:

The Simultaneous Inside Bar Break Indicator is a powerful tool for traders using The Strat methodology, offering a highly specific and reliable signal that can indicate potential large market moves. By monitoring multiple symbols and timeframes, you can gain deeper insight into the market's behavior and act with greater confidence. This indicator is ideal for traders looking to catch high-conviction moves and align their trades with broader market continuity.

Note: The indicator works best when paired with multi-timeframe analysis, allowing you to see how breaks on lower timeframes might influence larger trends. For traders who prefer simplicity, setting it to the "Chart Timeframe" mode offers flexibility while maintaining the core benefits of this indicator.

Multi-Step FlexiSuperTrend - Indicator [presentTrading]This version of the indicator is built upon the foundation of a strategy version published earlier. However, this indicator version focuses on providing visual insights and alerts for traders, rather than executing trades. This one is mostly for @thorcmt.

█ Introduction and How it is Different

The **Multi-Step FlexiSuperTrend Indicator** is a versatile tool designed to provide traders with a highly customizable and flexible approach to trend analysis. Unlike traditional supertrend indicators, which focus on a single factor or threshold, the **FlexiSuperTrend** allows users to define multiple levels of take-profit targets and incorporate different trend normalization methods.

It comes with several advanced customization features, including multi-step take profits, deviation plotting, and trend normalization, making it suitable for both novice and expert traders.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The **Multi-Step FlexiSuperTrend** works by calculating a supertrend based on multiple factors and incorporating oscillations from trend deviations. Here’s a breakdown of how it functions:

🔶 SuperTrend Calculation

At the heart of the indicator is the SuperTrend formula, which dynamically adjusts based on price movements.

🔶 Normalization of Deviations

To enhance accuracy, the **FlexiSuperTrend** calculates multiple deviations from the trend and normalizes them.

🔶 Multi-Step Take Profit Levels

The indicator allows setting up to three take profit levels, which are displayed via price level alerts. lows traders to exit part of their position at various profit intervals.

For more detail, please check the strategy version - Multi-Step-FlexiSuperTrend-Strategy:

and 'FlexiSuperTrend-Strategy'

█ Trade Direction

The **Multi-Step FlexiSuperTrend Indicator** supports both long and short trade directions.

This flexibility allows traders to adapt to trending, volatile, or sideways markets.

█ Usage

To use the **FlexiSuperTrend Indicator**, traders can set up their preferences for the following key features:

- **Trading Direction**: Choose whether to focus on long, short, or both signals.

- **Indicator Source**: The price source to calculate the trend (e.g., close, hl2).

- **Indicator Length**: The number of periods to calculate the ATR and trend (the larger the value, the smoother the trend).

- **Starting and Increment Factor**: These adjust how reactive the trend is to price movements. The starting factor dictates how far the initial trend band is from the price, and the increment factor adjusts subsequent trend deviations.

The indicator then displays buy and sell signals on the chart, along with alerts for each take-profit level.

Local picture

█ Default Settings

The default settings of the **Multi-Step FlexiSuperTrend** are carefully designed to provide an optimal balance between sensitivity and accuracy. Let’s examine these default parameters and their effect on performance:

🔶 Indicator Length (Default: 10)

The **Indicator Length** determines the lookback period for the ATR calculation. A smaller value makes the indicator more reactive to price changes, but may generate more false signals. A longer length smooths the trend and reduces noise but may delay signals.

Effect on performance: Shorter lengths perform better in volatile markets, while longer lengths excel in trending markets.

🔶 Starting Factor (Default: 0.618)

This factor adjusts the starting distance of the SuperTrend from the current price. The smaller the starting factor, the closer the trend is to the price, making it more sensitive. Conversely, a larger factor allows more distance, reducing sensitivity but filtering out false signals.

Effect on performance: A smaller factor provides quicker signals but can lead to frequent false positives. A larger factor generates fewer but more reliable signals.

🔶 Increment Factor (Default: 0.382)

The **Increment Factor** controls how the trend bands adjust as the price moves. It increases the distance of the bands from the price with each iteration.

Effect on performance: A higher increment factor can result in wider stop-loss or trend reversal bands, allowing for longer trends to develop without frequent exits. A lower factor keeps the bands closer to the price and is more suited for shorter-term trades.

🔶 Take Profit Levels (Default: 2%, 8%, 18%)

The default take-profit levels are set at 2%, 8%, and 18%. These values represent the thresholds at which the trader can partially exit their positions. These multi-step levels are highly customizable depending on the trader’s risk tolerance and strategy.

Effect on performance: Lower take-profit levels (e.g., 2%) capture small, quick profits in volatile markets, while higher levels (8%-18%) allow for a more gradual exit in strong trends.

🔶 Normalization Method (Default: None)

The default normalization method is **None**, meaning the deviations are not normalized. However, enabling normalization (e.g., **Max-Min**) can improve the clarity of the indicator’s signals in volatile or choppy markets by smoothing out the noise.

Effect on performance: Using a normalization method can reduce the effect of extreme deviations, making signals more stable and less prone to false positives.

Higher Time Frame Strat [QuantVue]The Higher Time Frame Strat Indicator is a tool that helps traders visualize and analyze price action from a higher timeframe (HTF) on their current chart. It applies the Strat method, a trading strategy focused on identifying key price action setups by observing how current price bars relate to previous ones. This helps in understanding the market's structure and determining potential trading opportunities based on higher timeframe data.

Key Concepts:

Strat Basics:

Type 1 Bar (Inside Bar): The current bar's high is lower than the previous bar's high, and its low is higher than the previous bar's low. This signifies a consolidation, or indecision, as the price is contained within the previous bar's range.

Type 2 Bar (Directional Bar): The current bar either breaks above the previous bar's high (bullish) or stays above the previous bar's low (bearish), indicating a continuation in the price direction.

Type 3 Bar (Outside Bar): The current bar breaks both above the previous bar's high and below the previous bar's low, showing volatility and a potential reversal.

Higher Timeframe Visualization:

The indicator uses a user-defined higher timeframe (default: 1 hour) and plots the last three higher timeframe candles on the current chart.

Strat Classification:

When a new higher timeframe candle forms, the indicator draws a semi-transparent box around the candle's range (high to low), along with the Strat type label. This provides a visual cue to the trader about the structure of the newly formed candle and how it fits into the overall market movement.

The script classifies each higher timeframe candle as one of the Strat types (1, 2, or 3). Based on the relationship between the current candle and the previous candle's high/low, it assigns a label ("1", "2", or "3"), helping traders quickly identify the price action setup on the higher timeframe.

How to Use the Indicator:

Trend Continuation: Look for Type 2 bars, which indicate a continuation in the current trend. For example, a Type 2 up suggests the price is breaking above the previous high, potentially signaling further upward movement.

Reversals: Type 3 bars show increased volatility, where the price breaks both above and below the previous bar's range. This could indicate a reversal, so be prepared for a potential change in direction.

Consolidation: Inside bars (Type 1) signify a tightening range and can signal the beginning of a breakout once the price moves outside of the previous bar's high or low.

By combining these price action concepts with the visualization of higher timeframe data, traders can potentially get earlier entry and exits as a higher timeframe set up forms.

Post-Open Long Strategy with ATR-based Stop Loss and Take ProfitThe "Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit" is designed to identify buying opportunities after the German and US markets open. It combines various technical indicators to filter entry signals, focusing on breakout moments following price lateralization periods.

Key Components and Their Interaction:

Bollinger Bands (BB):

Description: Uses BB with a 14-period length and standard deviation multiplier of 1.5, creating narrower bands for lower timeframes.

Role in the Strategy: Identifies low volatility phases (lateralization). The lateralization condition is met when the price is near the simple moving average of the BB, suggesting an imminent increase in volatility.

Exponential Moving Averages (EMA):

10-period EMA: Quickly detects short-term trend direction.

200-period EMA: Filters long-term trends, ensuring entries occur in a bullish market.

Interaction: Positions are entered only if the price is above both EMAs, indicating a consolidated positive trend.

Relative Strength Index (RSI):

Description: 7-period RSI with a threshold above 30.

Role in the Strategy: Confirms the market is not oversold, supporting the validity of the buy signal.

Average Directional Index (ADX):

Description: 7-period ADX with 7-period smoothing and a threshold above 10.

Role in the Strategy: Assesses trend strength. An ADX above 10 indicates sufficient momentum to justify entry.

Average True Range (ATR) for Dynamic Stop Loss and Take Profit:

Description: 14-period ATR with multipliers of 2.0 for Stop Loss and 4.0 for Take Profit.

Role in the Strategy: Adjusts exit levels based on current volatility, enhancing risk management.

Resistance Identification and Breakout: